- April 12,2021

- -

- Jake Woodward

Constant Kelly Betting Bankroll Management

Many bettors can recognize the value in a particular sports betting market. But how do you know how much money to bet, taking advantage of the detected value and not risk more money than you should? To find out this, sports bettors apply many investment strategies. One of the most famous is the Kelly Criterion. Since its creation in the last century mid-50s by the mathematician John Kelly, this method has remained in force. Over time, variants of this method have been generated. Among them are the Kelly Constant and the Fractional Kelly. Kelly calculated that the proportion of the funds you must invest equals your advantage. Kelly's formula tells us the following:

[(Occurring Probability) x (Betting Odds) - 1] / (Betting Odds-1).

If we use the Kelly Criterion values to bet, we can say we are employing the "Full Kelly Criterion." This widely used strategy has some significant disadvantages. First, our betting bankroll can suffer abrupt changes. Indeed, your funds can go up or down quickly. Another Kelly method drawback occurs when we want to bet on several events at the same time. In this case, when adding each event, betting percentages could result in us having to bet our entire betting bankroll. One way to avoid this is to use a more conservative method. That is, betting lower amounts than those indicated by the formula. In this sense, some Full Kelly Criterion variants propose using a portion of the percentage calculated by this method. One of these betting bankroll management systems is Constant Kelly.

The Constant Kelly In Sports Betting

This Kelly method variation works the same as the traditional method. But, in this case, we will not directly multiply the percentage obtained through Kelly's formula to our betting bankroll. Instead, we will multiply that percentage by a constant or fixed value. This constant will be a proportion of our betting bankroll previously established by the bettor. Instead of betting 17% of a variable amount like our betting bankroll, we will bet 17% of a fixed amount. This fixed value will be a fraction of our funds and can be, for example, between 0 and 0.5. In this way, we will be placing a kind of cap that will protect us from falling into bankruptcy if we apply the full Kelly criterion and have a bad streak. Let's see this method version through an example. Suppose we want to bet on the victory of a team whose odds are 2.1. Besides, we determined that it has a 60% winning probability. By using Kelly's formula, we will obtain:

((0.6 x 2.1) - 1) / (2.1 - 1) = 23.64%

We should bet almost a quarter of all our funds on that event. This may seem reckless to many punters. Thus, if we apply the constant Kelly and use, for example, 0.25 as a constant value, we will have:

0.25 x 23.64% = 5.91%

So, we will bet only 5.91% of our betting bankroll. This figure is a much more reasonable figure for any bettor. This full Kelly Criterion variant is much less aggressive in terms of the amounts to bet. Therefore, it is suited to punters looking for long-term profits while preserving their betting bankroll value. However, we must accurately estimate each event occurring probabilities to have success.

- Sports Industry Preview

- Soccer League Preview

- Profitable Trends

- Betting Guide

- Betting Help

- Betting Strategy

- Betting System

- Sports Betting

- World Cup

- Betting Tipsters

- Betting Bankroll

- Transfer Window

- Premier League

- Match Reviews

- Footballer Reviews

- Betting Predictions

- Club Reviews

- Manager Reviews

- Betting Odds

- Promotion Reviews

- Betting Trends

- Soccer Betting Tips Video Series

- English Football

- eSports

- Arsenal

- Borussia Dortmund

- Inter milan

- Betting Tips

- World Cup 2018

- Russia

- Italy

- Betting Expert

- Cristiano Ronaldo

- Lionel Messi

- Real Madrid

- France

- Belgium

- Brazil

- Germany

- Paul Pogba

- Marcos Ao??s Corr??a

- Timo Werner

- Aleksandr Golovin

- Sergej Milinkovic-Savic

- Alireza Jahanbakhsh

- Pione Sisto

- Denis Zakaria

- Soccer Tipsters

- Manchester United

- Hull City

- Abou Diaby

- Luc Nilis

- David Busst

- Ryan Mason

- English Premier League

- Middlesbrough F.C.

- Norwich City F.C.

- Sheffield Wednesday F.C.

- Bet Strategy

- Mix Parlay

- AS Monaco FC

- Goal Scoring Trends

- French Ligue 1

- Stade Malherbe Caen

- Stade Rennais F.C.

- Scottish Premier League

- Hibernian F.C.

- Dundee F.C.

- Kilmarnock F.C.

- Celtic F.C.

- Aberdeen F.C.

- Rangers F.C.

- Premier League

- Manchester City

- Barcelona

- FC Bayern Munich

- Carabao Cup

- Real Sociedad

- La Liga

- CD Legan??s

- Deportivo de La Coru?a

- Harry Kane

- England

- Steven Gerrard

- Juventus

- Mohamed Elyounoussi

- Danny Welbeck

- Mattia De Sciglio

- Viniciul Junior

- Flamengo

- Jose Mourinho

- Sir Alex Ferguson

- Chelsea

- Eden Hazard

- Jorginho

- Croatia

- Professional Punters

- Soccer betting tips

- Value Bets

- Betting Odds

- Mark Hughes

- Sportsbook

- Points per game

- PPG

- PPG statistics

- A.S. Roma

- Arsenal F.C.

- Tottenham Hotspur F.C.

- Liverpool F.C.

- Everton F.C.

- FK Partizan

- FK Crvena zvezda

- FC Schalke 04

- A.C. Milan

- Club Atl??tico River Plate

- Derby Della Capitale

- North London Derby

- Merseyside derby

- Eternal Derby

- Ruhr Derby

- Derby della Madonnina

- Superclasico

- World Cup 1998

- Japan

- Colombia

- Denmark

- Euro 2016

- Moscow

- Kaliningrad

- Saint Petersburg

- Nizhny Novgorod

- FC Basel

- Newspaper Betting Tipsters

- Television Betting Tipsters

- Radio Betting Tipsters

- Internet Betting Tipsters

- Soccer Betting Bankroll

- Soccer Betting Expert

- Pierre-Erick Aubameyang

- Fantasy Premier League

- Marko Arnautovic

- Wilfred Zaha

- Chris Wood

- Kyle Walker

- Cezar Azpilicueta

- Seamus Coleman

- Trent Alexander-Arnold

- Sol Bamba

- Leon Goretzka

- Jose Gimenez

- Max Meyer

- Jurgen Klopp

- Stoke City

- Coventry City F.C.

- Bookies

- Bonuses

- Alisson Becker

- Eliquim Mangala

- Anthony Martial

- Luke Shaw

- Toby Alderweireld

- Cesc Fabregas

- Ander Herrera

- Oliver Giroud

- Atletico Madrid

- Sevilla FC

- Ronaldo

- Van Nistelrooy

- Sunderland A.F.C.

- Betting Accumulators

- Mohamed Salah

- Indian Super League

- Pep Guardiola

- Livescores

- Golden Generation

- World Cup 2006

- SSC Napoli

- David De Gea

- Nick Pope

- Allison Becker

- Lukasz Fabianski

- Hugo Lloris

- Ederson Moraes

- VAR

- Dirk Kuyt

- Diego Milito

- Park Ji-Sung

- Thomas Muller

- Soccer Betting Facts

- 1X2

- Handicap Betting

- Total Goals

- SoccerTipsters

- Free Soccer Predictions

- Live Betting

- Bookmaker

- World Cup

- Qatar 2022

- PSG

- Ngolo Kante

- Claude Makelele

- American Football

- E-Sports

- Kathmandu Stadium

- Hillsborough

- CTE

- Chronic Traumatic Encephalopathy

- FIFA

- European Super League

- UEFA

- Neymar

- Professional Footballer

- EPL

- Christian Pulisic

- Lance Armstrong

- Tonya Harding

- Black Sox

- Match Fixing

- Calciopoli

- Formula One Spygate

- Women World Cup

- Series A

- Georgio Chiellini

- Fiorentina

- Bundesliga

- European Handicaps

- Accumulator Bets

- Parlays

- Arbitrage Betting

- Progressive Betting

- Martingale

- Oscar's grind

- Paroli System

- Martindale System

- David Moyes

- Southampton

- Betting Blog

- FA Cup

- SPAL

- Sampdoria

- RB Leipzig

- Champions League

- Betting On Soccer

- Casino Betting

- Teaser Bet

- Betting Bankroll

- Kelly Criterion

- In Play Betting

- Hedging

- Betting Market

- Matched Betting

- Betting Exchange

- Labouchere

- Serie B

- Crotone

- Italy Serie B

- Serie C

- Simeon Nwankwo

- Cittadella

- Liverpool

- UEFA Champions League

- Match predictions

- Paris Saint-Germain

- Atalanta

- Valencia

- Serie A

- Staking method

- Proportional Betting

- Martingale System

- Fibonacci System

- Arbitrage

- Underdogs

- Betting On Underdogs

- Beat The Bookies

- soccer betting

- Spread Betting

- Opening Odds

- Closing Odds

- Betting advice

- Sports Betting Addiction

- Betting Disorder

- Sports Betting in Indonesia

- Indonesia

- Betting On Sports

- Sports Betting in Malaysia

- Ascot Sports

- Betting Guide

- Indo Odds

- Sports Betting In Thailand

- Thailand Sportsbook

- Thailand Casinos

- Asian Bookies

- In-play Betting

- Over/Under

- betting system

- Europa league

- Leicester City

- Benevento Calcio

- Olympics

- Euro Cup

- America Cup

- betting trends

- BTTS

- Villarreal CF

- Betting on Casino

- Casino

- House Edge

- bankroll

- bankroll management

- Betting Bankroll Management

- Coronavirus

- Betting Value

- Asian Handicap

- Parlay

- Betting Probability

- betting on draw

- soccer leagues

- Draw Bets

- Egyptian Premier League

- French Ligue 2

- English League Two

- Correct Score

- Double Chance

- Fixed Odds

- Sportsbook Review

- Bet365

- Statistical Trends

- Marcus Rashford

- Alexandre Lacazette

- Son Heung-Min

- Calvert-Lewin

- Richarlison

- bookmakers

- IMSports

- IMesports

- Betting strategies

- Betting Algorithm

- Invictus

- Accumulator Generator

- Betegy

- AFC Champions League

- Asian Football Champions League

- Galatasaray

- Turkey Super League

- Istanbul Basaksehir

- Trabzonspor

- tipsters

- Smart Punter

- UEFA Euro 2020

- FC Barcelona

- Barça

- Takefusa Kubo

- Hwang Hee-chan

- Takumi Minamino

- Sardar Azmoun

- Erling Haaland

- Jadon Sancho

- Ansu Fati

- Alphonso Davies

- Vinícius Júnior

- Erling Braut Haaland

- Pierre-Emerick Aubameyang

- German Super Cup

- French League Cup

- Constant Kelly

- Football Betting Tips

- Sports Betting Trading

- mathematical expectation

- expected value

- Asian Football Leagues

- Chinese Super League

- K League

- Bet On Corners

- Double Chance Betting

- Sportsbooks

- Red devils

- Betting bonuses

- Rollover

- Welcome Bonuses

- Gerard Deulofeu

- EFL Championship

- Ismaïla Sarr

- Sbotop

- Sbotop Magazine

- Tottenham Hotspur

- Gareth Bale

- Superstitions

- MAXBET

- SBOBET

- M8bet

- Robert Lewandowski

- Odd And Even

- Pinnacle Sports

- Positive Progression

- Bettorclub

- Corner Kicks

- Sheffield United

- Luis Muriel

- Deportivo Cali

- Yankee Bet

- Trixie Combo Bet

- Underdogs Parlay

- Negative Progression

- d'Alembert

- Kevin De Bruyne

- Luka Modric

- Sergio Busquets

- Tony Cross

- Miralem Pjanic

- Frankie de Jong

- Casino games

- Online Slot

- Slot Machine

- RTP

- Romelu Lukaku

- Karim Benzema

- Wayne Rooney

- Derby County

- Dusan Vlahovic

- Vinicius Jr

- MLS

- New England Revolution

- Carles Gil

- Crystal Palace

- Conor Gallagher

- 3-Way Handicap

- Ferran Torres

- Xavi Hernández

- Gabriel Martinelli

- Transfer windows

- Kylian Mbappé

- Franck Kessié

- Ousmane Dembélé

- Paulo Dybala

- Sergio Aguero

- Independiente de Avellaneda

- Diego Maradona

- Luis Díaz

- Trent Alexander Arnold

- Bayern Munich

- Emile Smith Rowe

- Overwatch

- First Person Shooter

- eSports Betting

- Blackjack

- Insurance Bets

- Jude Bellingham

- Sadio Mané

- Jamal Musiala

- Goalkeepers

- Manuel Neuer

- Gianluigi Donnarumma

- Thibaut Courtois

- Nottigham Forest

- Gleison Bremer

- Torino FC

- Hajduk Split

- Torcida Split

- Bayern Leverkusen

- Frenkie de Jong

- Aurélien Tchouaméni

- Tiémoué Bakayoko

- Freiburg

- Nico Schlotterbeck

- Acca

- Betting Algorithms

- Algorithm

- Statistical Betting

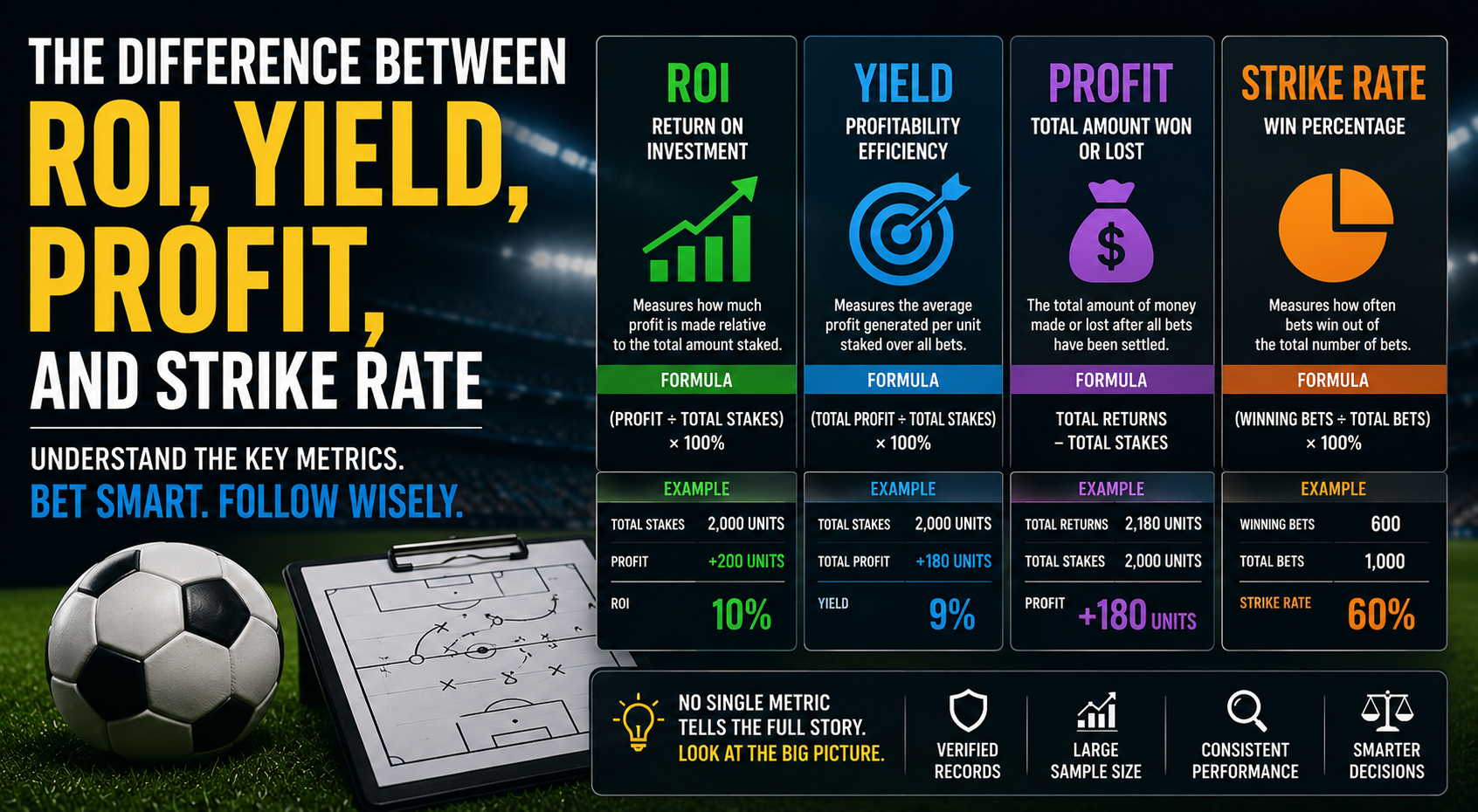

- Return On Investment

- ROI

- Betting Markets

- Decimals Odds

- Fractions Odds

- Handicap Odds

- Accumulator Bet

- Relegation

- Both Teams To Score

- Head-To-Head

- Goals Scored

- Dutching

- Early Cashout

- Accumulator Betting

- Over 1.5 Goals

- Total Goal

- Betting Formula

- Decimal Odds

- Both Team To Score

- Underdog

- Goal Scorer System

- Scoreline Betting System

- Handicap Betting System

- Positive Progression System

- Betting Tipsters

- Sports Prediction

- CMD368

- Bookie

- Sports Bookie

- Tipster

- Betting Tipster

- Cover a Bet

- Bet Against Yourself

- Money Management Strategy

- Handicapping Skills

- Handicapping

- Heinz System

- Martingale Betting

- Round Robin

- 1-3-2-6 System

- D’Alembert System

- Predictions

- Betting Exchanges

- Soccer Betting Mistakes

- Betting Mistakes

- Statistical Analysis

- Team Statistics

- Betting Data And Stats

- Historical Results

- Data Driven Strategies

- Sports Analytics

- Analytics

- Sports Betting Analytics

- Betting Analytics

- Deciphering Betting Odds

- Comprehending Betting Odds

- Probability

- Fractional Odds

- Money Line

- Futures Bet

- Prop Bet

- Goliath Bet

- Data Analysis

- Statistics And Data Analysis

- Historical Performances

- Statistical Evaluations

- Betting Strategy

- Betting Model

- Moneyline

- Prop Bets

- Major League Soccer

- Data Management

- 1X On Home

- Fibonacci Strategy

- Martingale Strategy

- Historical Performance

- Sports Betting Misconceptions

- Sports Betting Myths

- Soccer Betting Strategy

- Mathematical

- Statistical Model

- Advanced Analytics

- Performance Indicators

- Predictive Models

- Expected Goals

- Performance Analysis

- Bankroll Goals

- Stop-Loss Strategies

- International Friendly

- Per 90s

- Shooting Percentage

- Ball Possession

- xGChain

- Value Bet

- Compare Odds

- Bet Tracking

- Identifying Trends

- Betting Patterns

- In-Play Bet

- Single Handicap

- Double Handicap

- Quarter Handicap

- Analyzing Statistics

- Historical Data

- Expert Tipster

- Betting Prediction

- Draw No Bet

- Draw Betting

- Data-Driven

- Prop Betting

- Corners

- Own Goal

- Losing Streaks

- Emotional Management

- Analytical Tools

- Fantasy Soccer

- Fantasy Sports

- American Odds

- Implied Probability

- Betting Portfolio

- Diversified Betting Portfolio

- Betting Yield

- Each Way Betting

- Time Management

- Successful Sports Betting

- Head-to-Head Betting

- Lay Betting

- Stacking Techniques

- Stacking

- Insurance Betting System

- Mathematical Betting

- Statistical Analysis And Distributions

- Regression Analysis

- Statistical Significance

- Probability Distributions

- Bayesian Network

- Poisson Distribution

- Binomial Distribution

- Hedge Betting

- Return to Player

- Malaysian Sports Betting

- Form And Statistics

- Leeds United

- Howard Wilkins

- Marco Bielsa

- Malaysia

- Football Betting

- Badminton Betting

- Horse Racing

- Malaysian Super League

- Johor Darul Ta’zim FC

- Sri Pahang FC

- Persatuan Bolasepak Selangor FC

- Psychology Of Betting

- Risk-Taking

- Political Bet

- Indian Football Betting

- Market Trends

- Malaysian Odds

- Betting Formats

- Negative Odds

- Positive Odds

- Mobile Betting

- Artificial Intelligence

- Pritam Kotal

- ATK Mohun Bagan

- Malaysia Online Betting

- Betting Software

- Online Casino

- Wewin

- Slot

- Soccer Tipster

- Data Analytics

- Player Statistics

- Data and Analytics

- Flat Betting

- Eredivisie

- England Championship

- Cash-Out

- Pre-Match Betting

- Margin

- Shots on Target

- Possession Percentage

- Set Piece Stats

- Form Guide

- Line Movement

- Odds Comparison

- Standard Line Movement

- Reverse Line Movement

- Betting Tools

- OddsPortal

- Understat

- Flashscore

- BetStamp

- DNB

- Ligue 1

- Odds Movement

- Sharp Money

- Fake Tipster

- Scam Tipster

- Winning Streaks

- Chasing Losses

- Betting Records

- Betting Screenshots

- Market Liquidity